📌 यह Tax Planning Series का चौथा post है।

⚠️ सबसे पहले यह जानें

Section 80C का benefit सिर्फ Old Tax Regime में मिलता है। New Tax Regime choose करने वाले taxpayers Section 80C deduction claim नहीं कर सकते। अगर आप New Regime में हैं — यह post आपके लिए relevant नहीं है।

March आने पर एक सवाल हर salaried person के मन में आता है — “अभी तक ₹1.5 लाख का 80C पूरा नहीं हुआ — जल्दी से कहाँ invest करूँ?”

यह approach गलत है। 80C के instruments का चुनाव tax saving के लिए नहीं — अपने goals, liquidity need, और risk profile के हिसाब से होना चाहिए। Tax benefit एक bonus है, primary reason नहीं।

आज इसी सोच के साथ हर 80C option को honestly देखते हैं।

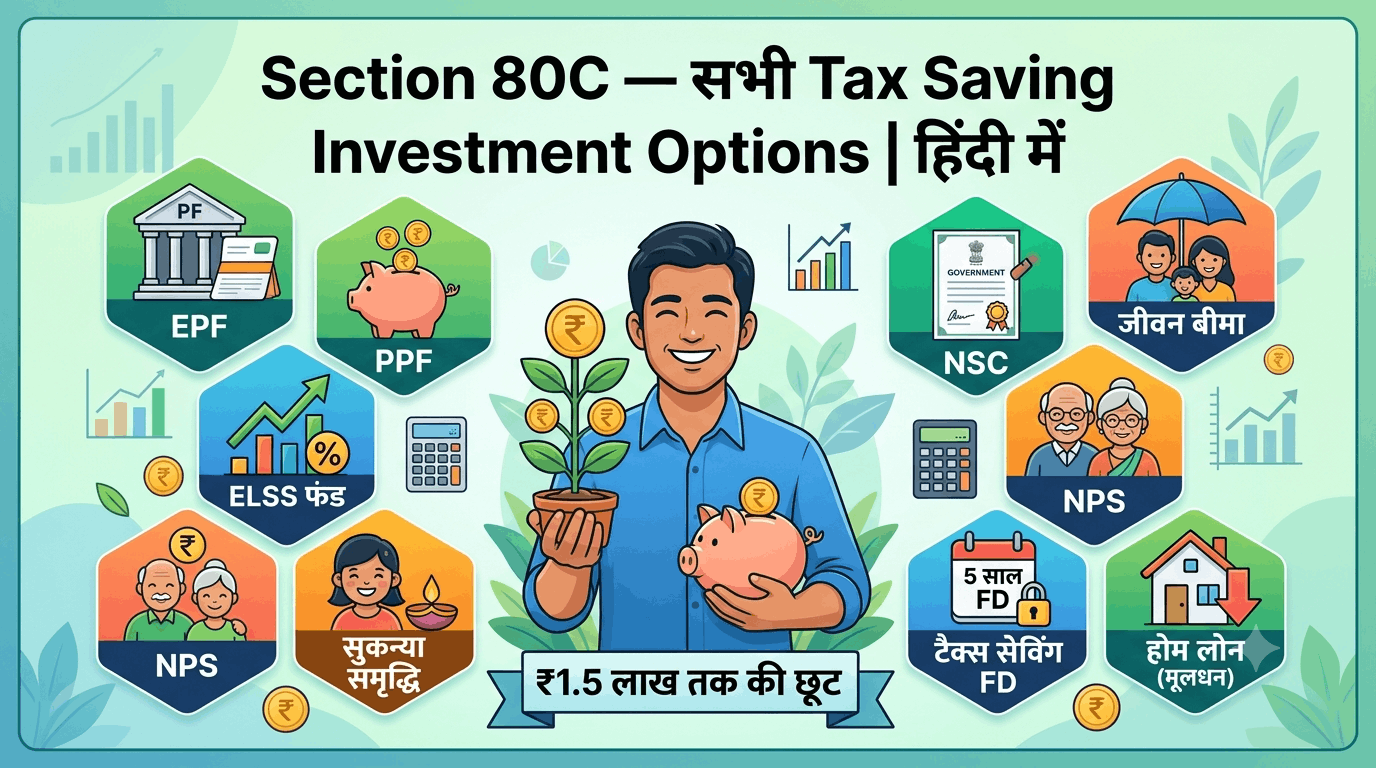

Section 80C — Basic Rules

₹1.5L

Maximum deduction limit — FY 2025-26 में unchanged

+₹50K

NPS में extra — Section 80CCD(1B) के तहत

Old Only

New Tax Regime में उपलब्ध नहीं

Combined Limit: ₹1.5 लाख सब मिलाकर है — PPF में ₹60,000 + ELSS में ₹50,000 + LIC में ₹60,000 = ₹1,70,000 invest किया तो भी deduction सिर्फ ₹1,50,000। ₹20,000 extra invest पर कोई extra tax benefit नहीं।

80C के सभी Options — एक नज़र में

| Option | Returns | Lock-in | Risk | Tax on Returns |

|---|---|---|---|---|

| PPF | 7.1% | 15 साल | Zero | EEE — Tax Free |

| ELSS Fund | 12-15%* | 3 साल | High | LTCG 12.5% (₹1.25L exempt) |

| EPF (Employee) | 8.25% | Retirement | Zero | EEE — Tax Free |

| Tax-Saving FD | 6.5-7.5% | 5 साल | Zero | EET — Interest Taxable |

| NSC | 7.7% | 5 साल | Zero | EET — Interest Taxable |

| Sukanya Samriddhi | 8.2% | 21 साल† | Zero | EEE — Tax Free |

| Life Insurance Premium | 4-6%** | Policy term | Low | Conditions apply |

| Home Loan Principal | N/A | Ongoing | — | N/A (expense) |

| Children Tuition Fees | N/A | N/A | — | N/A (expense) |

*Historical average, market-linked, not guaranteed | **Traditional plans — term insurance returns vary | †Girl child के 18 साल पर partial withdrawal, 21 साल पर maturity

Top 4 Options — Deep Dive

📱 80C Investments Track करें

ELSS SIP broker apps पर, PPF Post Office या SBI/HDFC app पर:

Recommended Strategy — Goal-wise

| आप कौन हैं | Best 80C Mix |

|---|---|

| Young professional (25-35 yr), risk ok | ELSS 70% + PPF 30% — balance of growth and safety |

| Mid-career (35-50 yr), moderate risk | EPF (auto) + PPF + ELSS balance — all three split करें |

| Conservative / near retirement | PPF + Tax FD + SCSS (Senior Citizens) — stability priority |

| Girl child है (under 10 yr) | Sukanya Samriddhi (8.2%, EEE) — dedicated child fund |

| Home loan है | Principal repayment 80C में count करें — बाकी ELSS/PPF से fill करें |

2 Expenses जो अक्सर Ignore होती हैं

Home Loan Principal: Bank की loan statement में “Principal Repayment” column देखें — यह 80C में count होता है। Interest repayment अलग section (24b) में जाता है, principal 80C में। बहुत लोग यह forget करते हैं।

Children Tuition Fees: 2 बच्चों तक की full-time education की tuition fees 80C में आती है। School fees का वो हिस्सा जो “tuition” है — transport, uniform, meals नहीं। Original receipts रखें।

💰 80C Planning — April में शुरू करें, March में नहीं

SIP से invest करें — एकमुश्त March में नहीं। Systematic approach better returns देती है।

अक्सर पूछे जाने वाले सवाल

क्या EPF contribution 80C में automatically count होता है?

हाँ। Employee का own EPF contribution 80C में automatically count होता है। Employer का contribution नहीं — वो employer का expense है। Form 16 में EPF deduction दिखता है। High basic salary वाले employees का EPF contribution ही ₹1.5 लाख limit touch कर सकता है — इसलिए पहले EPF amount check करें, फिर बाकी instruments plan करें।

क्या LIC premium पर 80C मिलता है?

हाँ, LIC और कोई भी IRDAI-approved insurance company का life insurance premium 80C में आता है। Condition: premium sum assured के 10% से ज़्यादा नहीं होना चाहिए। लेकिन सिर्फ tax के लिए costly traditional LIC policy लेना wise नहीं है — Term Insurance लें जो सस्ती होती है और protection देती है। Term insurance premium भी 80C में आता है।

NPS से ₹50,000 extra deduction कैसे मिलता है?

Section 80CCD(1B) के तहत NPS Tier-1 में ₹50,000 का extra deduction ₹1.5 लाख की 80C limit से ऊपर मिलता है। मतलब 80C में ₹1.5 लाख + NPS में ₹50,000 = कुल ₹2 लाख deduction claim हो सकता है। 30% slab में यह ₹15,600 extra tax बचा सकता है। NPS में 60 साल तक lock-in होता है, लेकिन retirement planning के लिए यह additional ₹50,000 benefit worth it है।

📚 Tax Planning Series

Sarita Mishra

Stock Market Educator | 10+ Years Investing Experience

मेरा 80C approach सरल है — EPF automatically हो जाता है, ELSS SIP April से शुरू हो जाती है, और PPF में साल की शुरुआत में ही डाल देती हूँ। March की rush नहीं। ELSS इसलिए पसंद है क्योंकि सबसे कम lock-in है — और historically PPF से ज़्यादा return मिली है लंबे समय में।

⚠️ Disclaimer: यह post केवल educational purpose के लिए है। Tax rates FY 2025-26 के अनुसार हैं। Investment returns indicative हैं — guaranteed नहीं। Section 80C सिर्फ Old Tax Regime में available है। Personal tax advice के लिए qualified CA से सलाह लें।