→ हमारी Full Disclaimer पढ़ें

⚡ Quick Answer

Equity Fund = High risk, High return — long-term wealth के लिए। Debt Fund = Low risk, Stable return — short-term goals के लिए। Hybrid Fund = दोनों का mix — balanced approach। अपना goal और risk tolerance देखकर चुनें।

Mutual Fund में invest करने का decision हो गया।

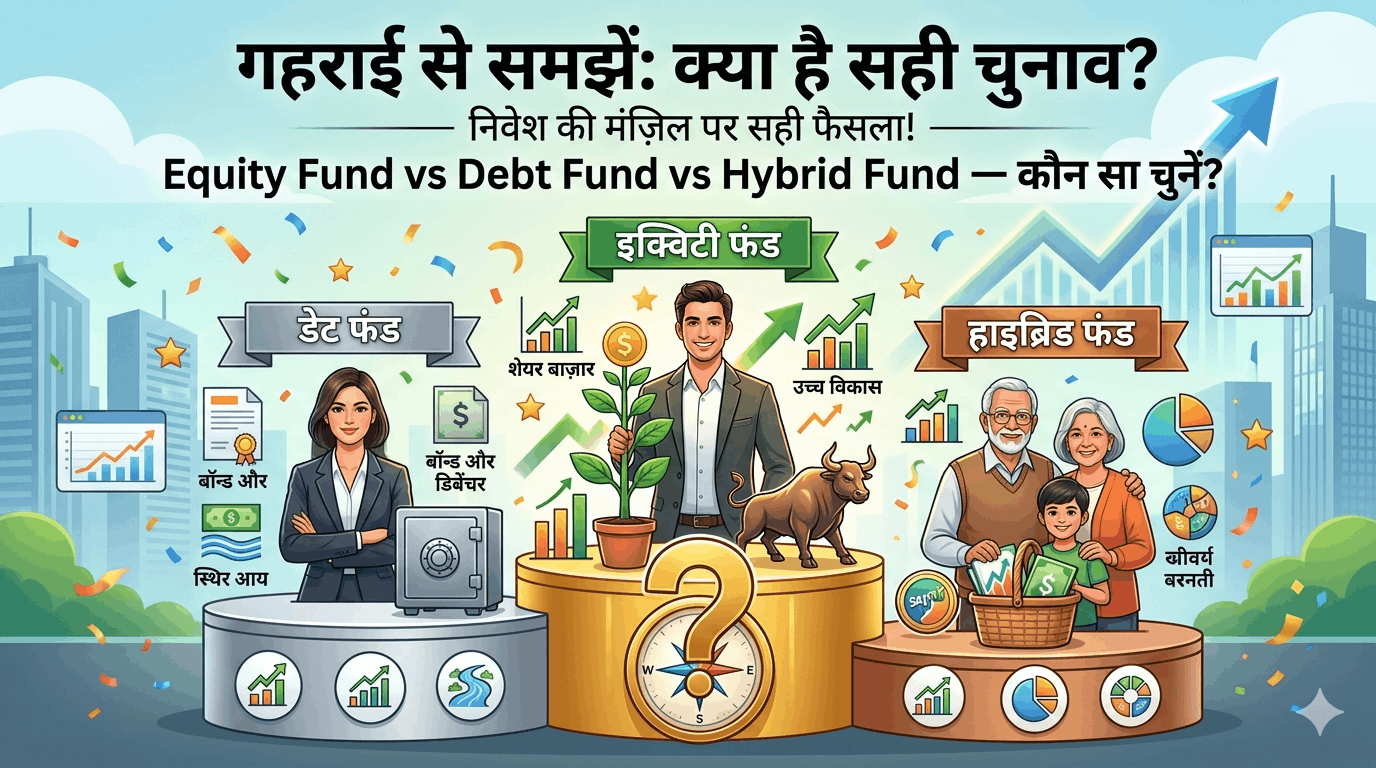

लेकिन अब अगला confusion आता है — “Equity Fund लूँ, Debt Fund लूँ, या Hybrid?”

तीनों के नाम सुने हैं — लेकिन फर्क क्या है? कौन सा आपके लिए सही है?

इस post में तीनों को honestly compare करूँगी — risk, return, tax, और कब कौन सा choose करें — सब कुछ clear हो जाएगा।

एक Line में तीनों का फर्क

📈

Equity Fund

पैसा Stocks में जाता है।

High risk.

High return.

🏦

Debt Fund

पैसा Bonds में जाता है।

Low risk.

Stable return.

⚖️

Hybrid Fund

पैसा दोनों में जाता है।

Medium risk.

Medium return.

📈 Equity Fund — Detail में

Equity Fund में आपका पैसा companies के shares (stocks) में invest होता है। Fund manager carefully companies select करता है।

Equity Fund के प्रकार:

| Type | Invest करता है | Risk | Best For |

|---|---|---|---|

| Large Cap | Top 100 companies (TCS, Reliance) | Medium | Stable growth |

| Mid Cap | 101–250 rank companies | Medium-High | Higher growth |

| Small Cap | 251+ rank companies | High | Aggressive growth |

| Flexi Cap | All caps — fund manager decide करता है | Medium | Balanced equity |

| ELSS | Equity + Tax benefit (80C) | Medium-High | Tax saving + Growth |

✅ Equity Fund के फायदे

- Long-term में सबसे ज़्यादा return

- Inflation को beat करता है

- Compounding का पूरा फायदा

- ELSS में tax benefit

⚠️ Equity Fund के नुकसान

- Short-term में बड़ा loss हो सकता है

- Market crash में 40%+ गिर सकता है

- 5+ साल का commitment ज़रूरी

🎯 Equity Fund किसके लिए: जिनका goal 5+ साल दूर है, जो market volatility सह सकते हैं, और long-term wealth बनाना चाहते हैं।

🏦 Debt Fund — Detail में

Debt Fund में पैसा Government Bonds, Corporate Bonds, Treasury Bills, और Fixed Income securities में invest होता है। यह essentially loan देने जैसा है — government या companies को।

Debt Fund के प्रकार:

| Type | Duration | Best Use |

|---|---|---|

| Liquid Fund | 1 दिन से 91 दिन | Emergency Fund, STP शुरू करने के लिए |

| Short Duration | 1–3 साल | Short-term goals, FD alternative |

| Corporate Bond Fund | 2–4 साल | FD से बेहतर return चाहिए |

| Gilt Fund | 5–10 साल | Government bonds, safest debt option |

✅ Debt Fund के फायदे

- FD से ज़्यादा liquid

- Stable returns

- Market crash में safe

- Short-term goals के लिए best

⚠️ Debt Fund के नुकसान

- Equity जितना return नहीं

- Interest rate risk होता है

- Credit risk (corporate bonds)

- Inflation नहीं beat होती

🎯 Debt Fund किसके लिए: 1–3 साल के goals, Emergency Fund park करने के लिए, या portfolio में stability लाने के लिए।

📱 तीनों funds में invest करें — एक ही platform पर

Equity, Debt, Hybrid — सब एक जगह। Direct Plan, Zero Commission:

⚖️ Hybrid Fund — Detail में

Hybrid Fund में Equity और Debt दोनों होते हैं। Fund manager decide करता है कि कितना % equity में और कितना % debt में जाएगा।

Hybrid Fund के प्रकार:

| Type | Equity % | Debt % | Best For |

|---|---|---|---|

| Conservative Hybrid | 10–25% | 75–90% | Retirees, Risk-averse investors |

| Balanced Hybrid | 40–60% | 40–60% | Moderate investors |

| Aggressive Hybrid | 65–80% | 20–35% | Growth + stability दोनों चाहिए |

| Balanced Advantage (BAF) | Dynamic (market देखकर) | Dynamic | Beginners के लिए best hybrid |

💡 Balanced Advantage Fund (BAF) क्यों special है?

BAF automatically adjust करता है — market महँगी हो तो equity कम, debt ज़्यादा। Market सस्ती हो तो equity ज़्यादा, debt कम। यह rebalancing automatically होती है। Beginners के लिए ideal — timing की tension नहीं।

तीनों का Head-to-Head Comparison

| पहलू | Equity Fund | Debt Fund | Hybrid Fund |

|---|---|---|---|

| Risk | High | Low | Medium |

| Expected Returns | 10–15% (LT) | 6–8% | 8–12% |

| Ideal Horizon | 5+ साल | 1–3 साल | 3–5 साल |

| Volatility | बहुत ज़्यादा | बहुत कम | Moderate |

| Tax (1 साल बाद) | 10% LTCG | Income Tax slab | Equity-like (65%+ equity) |

| Inflation Beat | ✅ हाँ | ❌ मुश्किल | Generally हाँ |

| Best For | Wealth creation | Capital protection | Balanced growth |

Tax कैसे लगता है? — Important

| Fund Type | 1 साल से कम (STCG) | 1 साल से ज़्यादा (LTCG) |

|---|---|---|

| Equity Fund (65%+ equity) | 20% | ₹1.25L तक exempt, फिर 12.5% |

| Debt Fund | Income Tax slab rate | Income Tax slab rate |

| Hybrid Fund (65%+ equity) | 20% | ₹1.25L तक exempt, फिर 12.5% |

⚠️ Note: Debt Fund पर अब indexation benefit नहीं मिलता (2023 के बाद)। सभी gains आपकी income में जुड़ते हैं। High tax bracket वाले investors के लिए Equity Fund tax-efficient है। Tax rules बदलते रहते हैं — invest करने से पहले latest rules confirm करें।

आपके लिए कौन सा? — Goal के हिसाब से चुनें

🚀 Goal तय किया? अब Invest शुरू करें

Direct Plan, Zero Commission — 5 मिनट में KYC

अक्सर पूछे जाने वाले सवाल (FAQ)

Beginner के लिए Equity, Debt, या Hybrid — कौन सा first?

Beginners के लिए दो options best हैं: (1) Nifty 50 Index Fund — simple, low cost, proven। (2) Balanced Advantage Fund — automatic rebalancing, कम tension। दोनों में SIP से शुरुआत करें। जैसे experience बढ़े, Mid Cap या Small Cap add करें।

Debt Fund और FD में कौन बेहतर है?

Liquidity में Debt Fund बेहतर है — FD तोड़ने पर penalty लगती है, Debt Fund कभी भी redeem करें। Returns similar या थोड़े ज़्यादा हो सकते हैं। लेकिन tax अब दोनों पर slab rate से लगता है। अगर 1 साल से कम के लिए पैसे रखने हैं — Liquid Fund FD से बेहतर है।

Hybrid Fund में Equity और Debt का ratio खुद change कर सकते हैं?

Hybrid Fund में fund manager ratio decide करता है — आप नहीं। लेकिन आप खुद अलग-अलग funds में invest करके अपना ratio बना सकते हैं। जैसे 70% Equity Fund + 30% Debt Fund। इसे “DIY Hybrid” कह सकते हैं — ज़्यादा control मिलती है।

Market crash में कौन सा fund safe है?

Market crash में Debt Fund सबसे safe रहते हैं — especially Liquid Fund और Gilt Fund। Equity Fund crash में 30–50% गिर सकते हैं। Hybrid Fund बीच में रहते हैं। इसीलिए short-term पैसे Debt में रखें, long-term Equity में। Diversification guide यहाँ पढ़ें।

क्या तीनों में एक साथ invest कर सकते हैं?

हाँ, और यही ideal approach है। एक simple formula: Equity Fund (long-term goals) + Debt/Liquid Fund (emergency fund + short-term goals) + ELSS (tax saving)। इसे Core Portfolio कहते हैं। जैसे experience बढ़े, Hybrid या Sectoral funds add कर सकते हैं।

📚 Mutual Fund Series — पूरी पढ़ें

Sarita Mishra

Stock Market Educator | 10+ Years Investing Experience

मेरे portfolio में तीनों हैं — Equity SIP long-term wealth के लिए, Liquid Fund emergency के लिए, और ELSS tax saving के लिए। हर fund का अपना काम है — सब एक साथ मिलकर portfolio को strong बनाते हैं।

⚠️ Disclaimer: यह post केवल educational purpose के लिए है। Mutual Fund investments market risk के अधीन हैं। Tax rules बदल सकते हैं — latest rules के लिए CA से सलाह लें। इसमें दी गई कोई भी जानकारी SEBI registered investment advice नहीं है। Invest करने से पहले scheme documents पढ़ें और SEBI registered financial advisor से सलाह लें।